Toni Perätalo

Director, Fund Management

The firm LCOE of solar power has nearly halved in five years. In his blog, Toni Perätalo examines what IRENA's report on firm LCOE means for the competitiveness of renewable energy, baseload generation, and energy investments.

Intermittency has long been identified as the single biggest challenge to scaling renewable energy: the sun doesn’t shine at night, and the wind doesn’t blow on demand. Weather variability has given fossil fuel defenders an argument about renewables being unsuitable for producing baseload, on-demand around-the-clock electricity supply that modern societies depend on regardless of season or time of day.

In May 2026, the International Renewable Energy Agency (IRENA) published a report that challenges this view. 24/7 Renewables: The Economics of Firm Solar and Wind shows that solar and wind, combined with battery energy storage systems (BESS), can already deliver reliable and cost-competitive around-the-clock electricity in favourable conditions. In many cases, renewables now meet demand more cheaply than fossil-fuel power plants.

Can renewables meet the needs of critical infrastructure that requires a steady supply of electricity every hour of the year on-demand?

IRENA introduced a new metric to answer this question: firm LCOE, the levelised cost of firm renewable electricity.

Conventional LCOE measures the average cost of producing power from a standalone plant. Firm LCOE goes a step further: it is defined as the standalone LCOE plus a firming premium, the additional expenditure needed to meet a specified reliability target (set by default to 95 % in IRENA’s modelling). The firming premium includes the cost of everything required to turn renewable output into firm supply: battery energy storage, overbuilt generation capacity, and hybrid solutions combining solar and wind.

Understanding the cost of this “firming” is central to assessing renewable economics against other steady electricity generation cost.

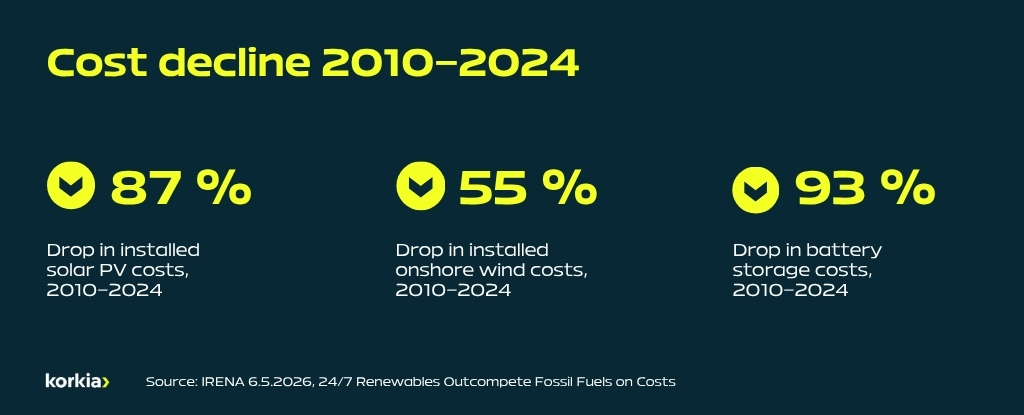

The backdrop to IRENA’s report is a decline in technology costs. Between 2010 and 2024, installed solar PV costs fell by 87 per cent. Onshore wind costs fell by 55 per cent over the same period. Battery storage costs dropped 93 per cent, and in 2025 prices continued to fall by roughly 30 per cent.

This decline is showing up directly in firm LCOE. In 2020, firm LCOE of solar power typically costs more than USD 100/MWh. By 2025, in the best solar resource zones, firm LCOE had already fallen to roughly USD 54–82/MWh, and by 2035 the best sites are projected to drop below USD 50/MWh.

China illustrates a market in which renewables are already cheaper than fossil generation. Solar paired with battery storage now clears below USD 100/MWh on a firm LCOE basis in a clear majority of projects, and at the low-end firm costs fall to around USD 30/MWh at a 90 per cent reliability level. A new coal-fired plant in China typically costs USD 70–85/MWh.

A concrete example comes from the United Arab Emirates, home to some of the world’s cheapest fossil fuel, where the UAE’s Al Dhafra complex already delivers a firm 1 GW of solar-plus-storage power at around USD 70 per MWh, a level that is competitive with gas-fired generation.

As demand from data centers, AI workloads, and electricity-intensive industry accelerates, hybrid systems are also competitive with the speed of deployment. A power plant with solar and storage can typically be built and brought online within one to two years of permits and grid connection being secured: significantly faster than new gas plants in many markets, with the contrast even sharper versus new nuclear.

Often projects that combine solar, wind, and BESS deliver firm renewable power affordably and quickly. Solar produces during the day, while wind tends to fill in at night and on overcast days. Combined with battery storage, hybrid systems can reach a 95 per cent reliability target at significantly lower cost than standalone solar or wind plants.

The 95 % reliability level is the default assumption used in IRENA’s modelling. A reliability target of 80–95 % is considered the most cost-effective “sweet spot” for hybrid plants, as costs rise sharply beyond that range. The remaining gap can be covered at the system level, through demand-side flexibility, dispatchable generation, transmission, and various forms of energy storage.

This report confirms what energy markets have been signaling for some time: the competitiveness of renewable energy no longer depends on political subsidies or exceptional circumstances.

It rests on technology development, scale, low costs, and relatively fast development and construction timelines.

At the same time, fossil-fuel supply security has weakened. The Strait of Hormuz crisis has disrupted nearly a fifth of global oil trade, causing oil and LNG prices to rise. With renewable prices falling and fossil prices climbing, the direction of travel is clear. The next question: where and when do we build?

Source: International Renewable Energy Agency (IRENA): 24/7 Renewables: The Economics of Firm Solar and Wind, Press release (6.5.2026)

Korkia clarifies its leadership structure as Mikko Kantero takes responsibility for portfolio execution and growth.

Korkia's Swedish renewable energy portfolio has received an environmental permit for a hybrid project in Smedjebacken, Dalarna.

Korkia and Evolution Power have achieved ready-to-build (RTB) status for the 150 MWp Stonestreet Green Solar and BESS project in Kent,...