Mikko Kantero

Executive Vice President, Portfolio Management & Growth

Finland, Italy and Chile show how the return potential of battery energy storages shifts with each market's stage of development.

Battery Energy Storage Systems (BESS) have become an indispensable building block of a sustainable power system. Storage is now required wherever the energy system is electrifying and the share of renewables on the grid is rising, reaching virtually every fast-evolving market from South America to the Nordics.

For investors, the moment is an unusual one: demand is scaling rapidly, the technology has matured at pace, and markets worldwide are opening on very different timelines.

A battery storage system is more than just a place to store energy. Storage assets match supply with demand, relieve grid congestion, provide balancing services, and deliver backup and regulating capacity. In doing so, they strengthen security of supply and enable a rapid response to shift in electricity demand.

The need for battery storage arises from two directions. Significant growth of solar and wind power has created a structural need to balance weather-dependent, intermittent generation. Solar projects now in planning are often paired with co-located BESS to firm up output.

At the same time, structural shifts such as the electrification of transport and industry, along with the construction of data centers, are driving electricity demand higher. The implications of data center load growth for the power system are currently the subject of active debate in many countries. Battery storage is also a critical component of the emerging data center ecosystem, helping to secure the power system of the future even as demand multiplies.

BESS is needed everywhere, but it is not a lucrative nor attractive investment everywhere. A battery storage business can be run through arbitrage, reserve markets, or energy time-shifting, or in the best case, all three. An investment decision depends on a range of factors that can be condensed into three areas.

Market and regulation. Local market structure and the prevailing regulatory regime are primary determinants of battery storage profitability. Conditions vary widely across jurisdictions: in the business models permitted, the maturity and predictability of permitting processes, and the transparency and stability of governance. A central question in any profitability assessment is the revenue mix. How much is underpinned by regulated, contracted income streams versus exposure to merchant, market-based revenue?

Anticipating the future. Because the BESS market is evolving at an accelerating pace, the forward view matters more than current conditions. Price volatility, the trajectory of capacity requirements, and regulatory developments can all be anticipated and modelled. A sound investment case rests on that outlook rather than on today’s spreads.

Project-level economics. Ultimately, each project stands on its own merits: demand at commissioning is a function of both broader market dynamics and asset-specific factors such as location, grid position, and timing. Early-stage development capital deployed into battery storage development typically targets a return of at least 3–4x, depending on the risk profile.

The global BESS market is made up of dozens of different markets, each at its own stage of development. Below are a few examples from three markets at very different stages:

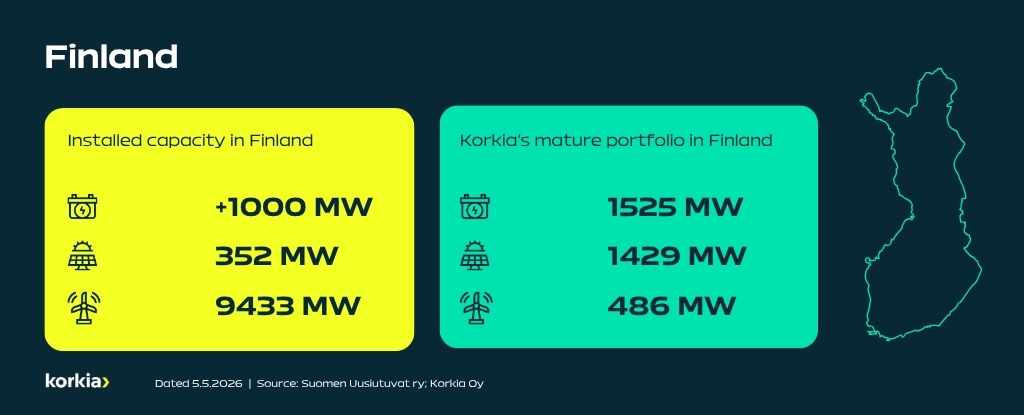

Market stage. By global standards, Finnish BESS market is mature and well advanced. Fingrid, Finland’s national TSO, projects that national electricity consumption could double by 2035, underpinning a robust long-term growth outlook. Continued build-out of wind and solar sustains and amplifies price volatility, creating an attractive operating environment for storage and broader energy investment. The regulatory regime for storage is permissive and enabling.

Revenue streams. Broad revenue stack is the key strength of Finnish BESS market. Assets monetise across the reserve market while capturing arbitrage spreads in both the day-ahead and intra-day markets.

Uniqueness. Persistently high price volatility, driven by rising wind and solar penetration, makes Finland a particularly strong arbitrage market.

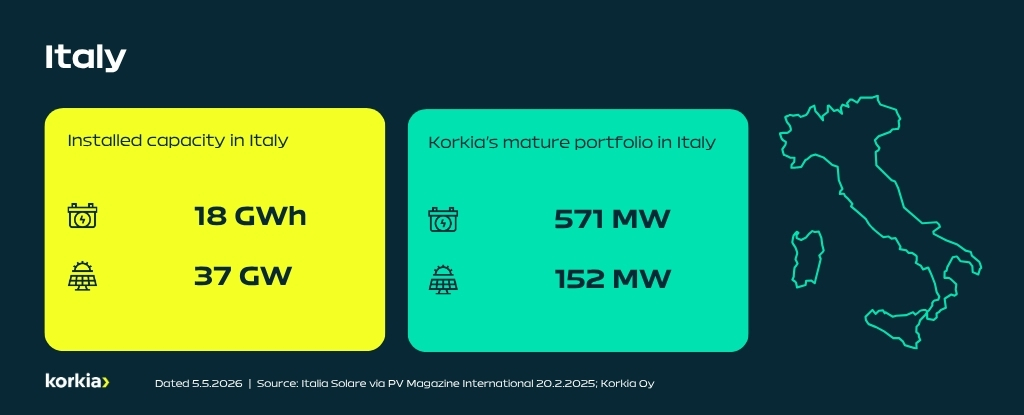

Market stage. In Italy, rapid renewable build-out is accelerating demand for storage, with strong growth expected for large-scale assets in 2026–2027. Returns from dispatching and peak management services are set to improve over the coming years.

Revenue streams. The revenue stack remains narrow for now, anchored largely in the capacity market, while arbitrage and reserve markets are still at an early stage of development.

Uniqueness. Accelerating renewable deployment is rapidly increasing the need for storage. A widening price spread between consumption peaks and overproduction periods creates excellent conditions for arbitrage returns as the market matures.

The upside lies in timing: returns from dispatching and peak management services will build over the coming years, and early movers can position themselves before the market matures.

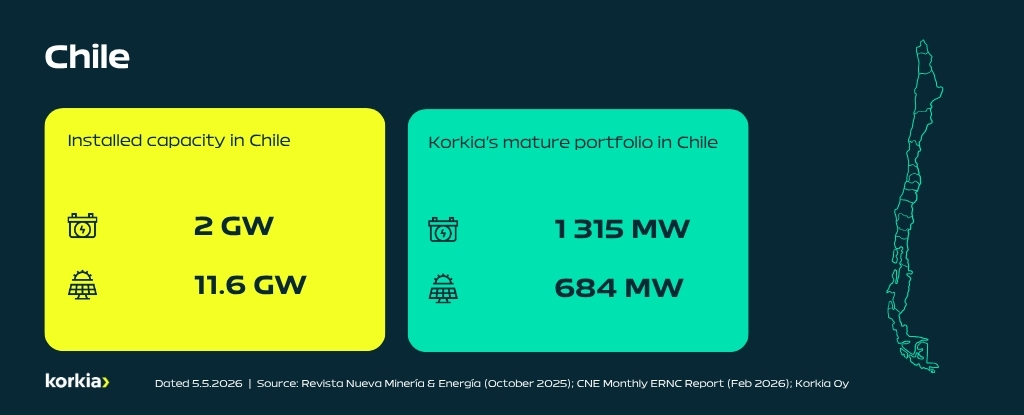

Market stage. The dynamism of the Chilean market is captured by a single data point: the national 2 GW storage target was met in early 2026, roughly four years ahead of schedule, with more than 6 GW already in the construction pipeline. Under the country’s nodal pricing system, asset location is a decisive value driver: the solar-rich north runs into oversupply while central demand nodes command higher prices, a spread that well-sited storage is built to capture.

Revenue streams. Arbitrage and capacity services markets are already established under Chile’s 2022 Energy Storage Law, and the reserve services market for battery storage (SSCC) is being formalised over the course of 2026.

Uniqueness. Chile’s development path diverges from most other markets. Grid operators are stepping directly into storage: transmission operator Transelec, for instance, is building and running a 105 MW battery for a generator under a build-own-operate-transfer (BOOT) model, owning the asset before eventually handing it over. This structure opens up business models distinct from traditional ownership.

What these very different markets share is direction: demand is rising, regulation is maturing, and revenue opportunities are broadening. The greatest rewards accrue to investors who read the market’s stage correctly and position themselves early.

Our team at Korkia actively follows the growth of battery storage markets around the world. We are currently developing battery storage projects in eight countries, including Finland, Italy and Chile.

Korkia clarifies its leadership structure as Mikko Kantero takes responsibility for portfolio execution and growth.

Korkia's Swedish renewable energy portfolio has received an environmental permit for a hybrid project in Smedjebacken, Dalarna.

Korkia and Evolution Power have achieved ready-to-build (RTB) status for the 150 MWp Stonestreet Green Solar and BESS project in Kent,...